又到咗每年行禮如儀攤大手板問尾帝拎返交多咗股息稅的季節。程序基本上跟往年一樣,有分別都只不過是小改動。先從Interactive Brokers(下稱 IB)下載 Form 1042-S:這份表格就係 IB 幫魔術師向 IRS 報稅的 breakdown;然後再下載 2021 年度的 dividend report(留意 IB 的 Dividend report 有 HTML 版和 CSV 版,魔術師要先打開 HTML 版,再將所有 subsections 打開,再手動 print 個 PDF 版出來備用) :

跟往時一樣,IB 在3月15日已經準備好 Form 1024-S,以下的 income code 都是不用繳稅,而且 IB 也已經在 2021 年年頭退回魔術師因以下原因多付了的 withholding tax :

- Income code 01 Interest paid by U.S. obligors - general - 債劵利息

- Income code 33 Substitute payment-interest - 借貨沽空方代支債劵利息

- Income code 36 Capital gain - 股息中含有資產增值的份額

- Income code 37 Return of capital - 股息中含有本金的份額

現在魔術師要申請退回的是屬於 ETF 派息中含有 Foreign Source Income(FSI) 及債劵利息(Qualified Interest Income, QII)等這些 Non-resident Alien (NRA) 可以免繳稅的項目,這些可退稅金額都是本來已經包含在以下 income codes 之內:

- income code 06 Dividends paid by U.S. corporations-general - 就是最普通的股息派發

- income code 34 Substitute payment-dividends - 借貨沽空方代支股息

現在的工作就是要將它們分拆出來。是否值得花功夫去鑽研這部份的可退稅金額因人而異,要視乎各人的投資項目及投資額而定。

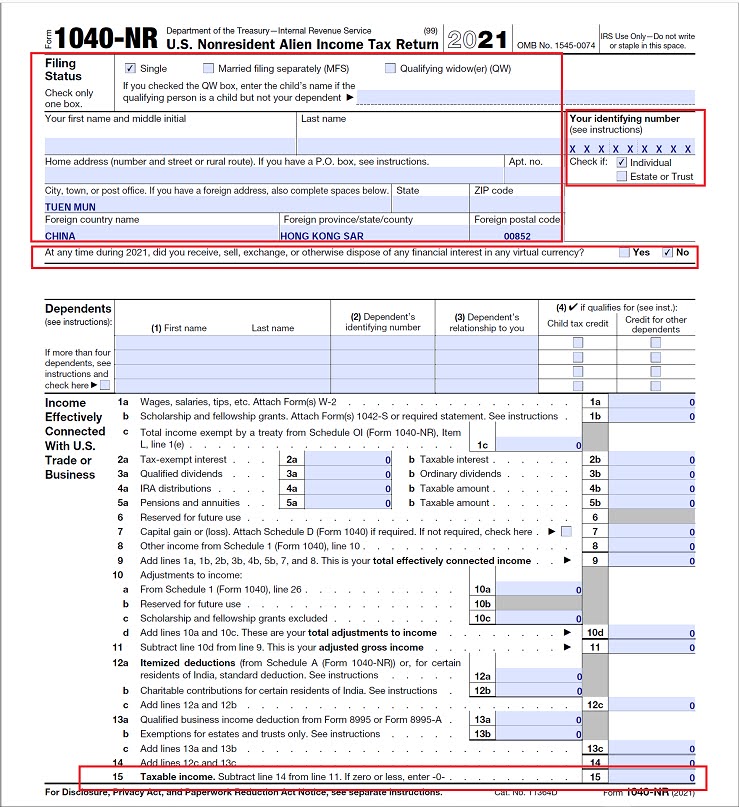

NRA 如果要申請退稅的話就要填 Form 1040-NR,由第一頁講起:

1. Effectively Connected Income(ECI):魔術師首先要考慮的是需唔需要報 Effecitvely Connected Income 的 tax return。由於魔術師早在2021年年結時便將 America First Multifamily Investor, L.P.(ATAX)沽清,其所收股息亦已交足37%的 Public Traded Partnership(PTP,income code 27) 股息稅,一季咁大把嘅股息魔術師就唔再做太複雜計算,放棄 ECI 的 tax refund,就當是豪俾佢。

2. Virtual Currency:根據 Instructions for Form 1040-NR (2021),

Virtual currency. See Virtual Currency in the Instructions for Form 1040.

再睇 Form 1040 (2021) Instructions:

Virtual Currency

Virtual currency is a digital representation of value, other than a representation of the U.S. dollar or a foreign currency (“real currency”), that functions as a unit of account, a store of value, or a medium of exchange. Some virtual currencies are convertible, which means that they have an equivalent value in real currency or act as a substitute for real currency. The IRS uses the term “virtual currency” to describe the various types of convertible virtual currency that are used as a medium of exchange, such as digital currency and cryptocurrency. Regardless of the label applied, if a particular asset has the characteristics of virtual currency, it will be treated as virtual currency for Federal income tax purposes.

If, in 2021, you engaged in any transaction involving virtual currency, check the “Yes” box next to the question on virtual currency on page 1 of Form 1040 or 1040-SR. A transaction involving virtual currency includes, but is not limited to:

- The receipt of virtual currency as payment for goods or services provided;

- The receipt or transfer of virtual currency for free (without providing any consideration) that does not qualify as a bona fide gift;

- The receipt of new virtual currency as a result of mining and staking activities;

- The receipt of virtual currency as a result of a hard fork;

- An exchange of virtual currency for property, goods, or services;

- An exchange/trade of virtual currency for another virtual currency;

- A sale of virtual currency; and

- Any other disposition of a financial interest in virtual currency.

A transaction involving virtual currency does not include the holding of virtual currency in a wallet or account, or the transfer of virtual currency from one wallet or account you own or control to another that you own or control. If your only transactions involving virtual currency during 2021 were purchases of virtual currency for real currency, including the use of real currency electronic platforms such as PayPal and Venmo, you are not required to check the “Yes” box next to the virtual currency question. You must not leave the field blank even if you are not required to answer “Yes”. If you disposed of any virtual currency that was held as a capital asset through a sale, exchange, or transfer, check “Yes” and use Form 8949 to figure your capital gain or loss and report it on Schedule D (Form 1040).

If you received any virtual currency as compensation for services or disposed of any virtual currency that you held for sale to customers in a trade or business, you must report the income as you would report other income of the same type (for example, W-2 wages on Form 1040 or 1040-SR, line 1, or inventory or services from Schedule C on Schedule 1).

For more information, go to IRS.gov/virtualcurrencyfaqs.

雖然話 "The receipt of new virtual currency as a result of mining and staking activities" 與及 "An exchange/trade of virtual currency for another virtual currency" 都需要報稅,但尾帝其實係將虛弊當成係 property 和 capital asset 等去處理。根據 Publication 519 (2021), U.S. Tax Guide for Aliens,裡面並無提及過 NRA 需要對經過尾帝境外交易所的虛弊交易報稅(non US source income),加上純投資交易係 non effectively connected,更何況就算係有 capital gain,都唔需要交稅:

Tax at a 30% (or lower treaty) rate applies to certain items of income or gains from U.S. sources but only if the items are not effectively connected with your U.S. trade or business.

:

:

:

The following gains are subject to the 30% (or lower treaty) rate without regard to the 183-day rule, discussed later.

- Gains on the disposal of timber, coal, or domestic iron ore with a retained economic interest.

- Gains on contingent payments received from the sale or exchange of patents, copyrights, and similar property after October 4, 1966.

- Gains on certain transfers of all substantial rights to, or an undivided interest in, patents if the transfers were made before October 5, 1966.

- Gains on the sale or exchange of OID obligations.

:

:

:

If you were in the United States for less than 183 days during the tax year, capital gains (other than gains listed earlier) are tax exempt unless they are effectively connected with a trade or business in the United States during your tax year.

所以魔術師就一於在 Form 1040-NR 第一頁的 Virtual Currency Transaction 中打「No」。

其餘個人資料、International Taxpayer Identification Number(ITIN,見《假扮美帝公民入領事館做公證(2017)》)等就照事實填寫:

要填 Form 1040-NR 第二頁,就先要填好 Form 1040-NR Schedule NEC Tax on Income Note Effectively Connected with a U.S. Trade or Business:

要填 Form 1040-NR 第二頁,就先要填好 Form 1040-NR Schedule NEC Tax on Income Note Effectively Connected with a U.S. Trade or Business:

4. Row 1a Dividends and dividend equivalents paid by U.S. Corporation, Column (d) 37%:直接抄 Form 1042-S Income code 27 Publicly traded partnership distributions subject to IRC section 1446 的 Box (2)。參考上圖例子就係$1,000。

5. Row 2c Interest (Other), Column (d) 0%:直接抄 Form 1042-S Income code 01 的 Box (2)。參考上圖例子就係$20,000。

6. Row 12 Other, Column (d) 0%:魔術師做完 research(見參考資料),得知以下兩隻持股的派息含 Foreign Source Income(多數為 International ETF)

- Vanguard Global ex-U.S. Real Estate ETF (VNQI):股息當中 65.513835% 為 Foreign Source Income,實際股息率為10.35%(=(100-65.513835)%x30%)。

- Vanguard Global ex-U.S. Real Estate ETF (VNQI):股息當中 100% 為 Foreign Source Income,實際股息率為0%(=(100-100)%x30%)。

再從上述的 IB Dividend Report 的 Dividend Detail section(對應 Form 1042-S Income code 06)及 Payment in Lieu Detail(對應 Form 1042-S Income code 34)中找到 HEDJ 及 VNQI 的派息及已收取的股息稅,再用 Excel 計返免稅部分,與及實際要付的股息稅,最後就係 Tax refund(舉例如下):

將上述 Excel 的 Foreign Source Income($396) 再加埋 Income codes 33, 36, 37的 Box (2)(分別為$2,000、$3,000、和$4,000),就可以得出修正後的免稅股息收入$9,396。

7. Row 1a Dividends and dividend equivalents paid by U.S. Corporation, Column (c) 30%:將 Form Income code 06 及 34的 Box (2)(分別和$5,600和$400) 加起來,就是原來用來 charge 30% 股息稅的基礎,現在計到有$396是免稅的 FSI,故此 Taxable income 就是$5,604(=6000-396)。

8. 最後,依算式將 Form 1040-NR Schedule NEC Lines 13、14、15 填好,經修正後要交的股息稅為$2,501。

9. 魔術師的虛弊交易全部都唔係 U.S. source income,故 Form 1040-NR Schedule NEC Lines 16、17、18 從略。

返回 Form 1040-NR 第二頁,

10. 將 Form 1040-NR Schedule NEC Line 15 抄入 Form 1040-NR Line 23a,並且計出 Line 23d。

11. 將原先 Form 1042-S 各 Income codes 的 Box (10) 加起來,就是總已交付股息$2,170(=370+120+1680),填入 Form 1040-NR Line 25g,並且計出 Line 33。

12. Form 1040-NR Line 34、35a 就係退稅部分,依上述例子,就可以取回$119(=2170-2051)。

13. 然後就係 Form 1040-NR Schedule OI Other Information,純粹事實陳述,依照個人情況申報就是,無需任何技巧。

14. 最後,簽好名,填好日期,再將 Form 1042-S、Form 1041-NR、Form 1041-NR Schedule NEC、Form 1041-NR Schedule OI、與及一眾 supporting documents 依 instruction 指示依次序疊好,便可以寄往

Individuals. If you are not enclosing a payment, mail Form 1040-NR to:

Department of the Treasury

Internal Revenue Service

Austin, TX 73301-0215

U.S.A.

If enclosing a payment, mail Form 1040-NR to:

Internal Revenue Service

P.O. Box 1303

Charlotte, NC 28201-1303

U.S.A.

以一般 NRA 來說,報稅的截止日期為2022年6月15日。

Individuals. If you were an employee and received wages subject to U.S. income tax withholding, file Form 1040-NR by the 15th day of the 4th month after your tax year ends. A return for the 2021 calendar year is due by April 18, 2022.

If you file after this date, you may have to pay interest and penalties. See Interest and Penalties, later.

If you did not receive wages as an employee subject to U.S. income tax withholding, file Form 1040-NR by the 15th day of the 6th month after your tax year ends. A return for the 2021 calendar year is due by June 15, 2022.

(註:筆者並非稅務專家,本文純屬基於心得分享,個人理解容或有錯,不能作為教學之用。讀者如有稅務問題,應請教有關專家為上。)

***

參考資料:

Publication 519 (2021), U.S. Tax Guide for Aliens

Internal Revenue Service: Instructions for Form 1040-NR (2021)

Internal Revenue Service: 1040 (2021)

Vanguard > TAX CENTER > 2021 TAX CALENDAR > Vanguard ICI 2021 Secondary layout spreadsheet

***

伸延閱讀:

謝謝分享。想請教一下如果是透過本地銀行(e.g. HSBC)持有美股,這些本地銀行好像不會向客戶發出1042S表格,對向美國政府claim 回多繳的withholding tax 會有影響嗎? 魔術師先生有這樣的經驗可以參考一下嗎?

回覆刪除我一向也是在IBHK 買賣美股並用它提供的1042S表格作為1040-NR (U.S. Nonresident Alien Income Tax Return) 的supporting documents 去claim 多繳了的witholding tax,但由於IBHK 沒有SIPC 500k USD insurance,再加上近期美國金融機構有擠提風險,所以有打算將資金由IBHK 取出再分散到多間銀行,但又擔心銀行不發1042S表格會影響我去claim 多繳了的witholding tax...

既然你不嬲有 claim 開 tax refund,應該知道沒有 1042-S 就 claim 不到 withholding tax refund. 完。

刪除好多年前我在大貓買過 VNQ, 佢好似隔咗兩年先 refund 疑似是withholding tax 中 ROC 的部份俾我,乜 detail 都無都唔知有無計錯數。如果係債基 或 foreign source income 大貓應該無 refund withholding tax 的。